Alternatives Are Like Portfolio Supplements: The Right Ones Help. The Wrong Ones Hurt.

If you missed it, Consumer Reports (“CR”) dropped a bombshell on the nutrition and fitness industry a few weeks ago.

After testing 23 popular protein powders, they found that almost all contained alarming levels of lead and other heavy metals.

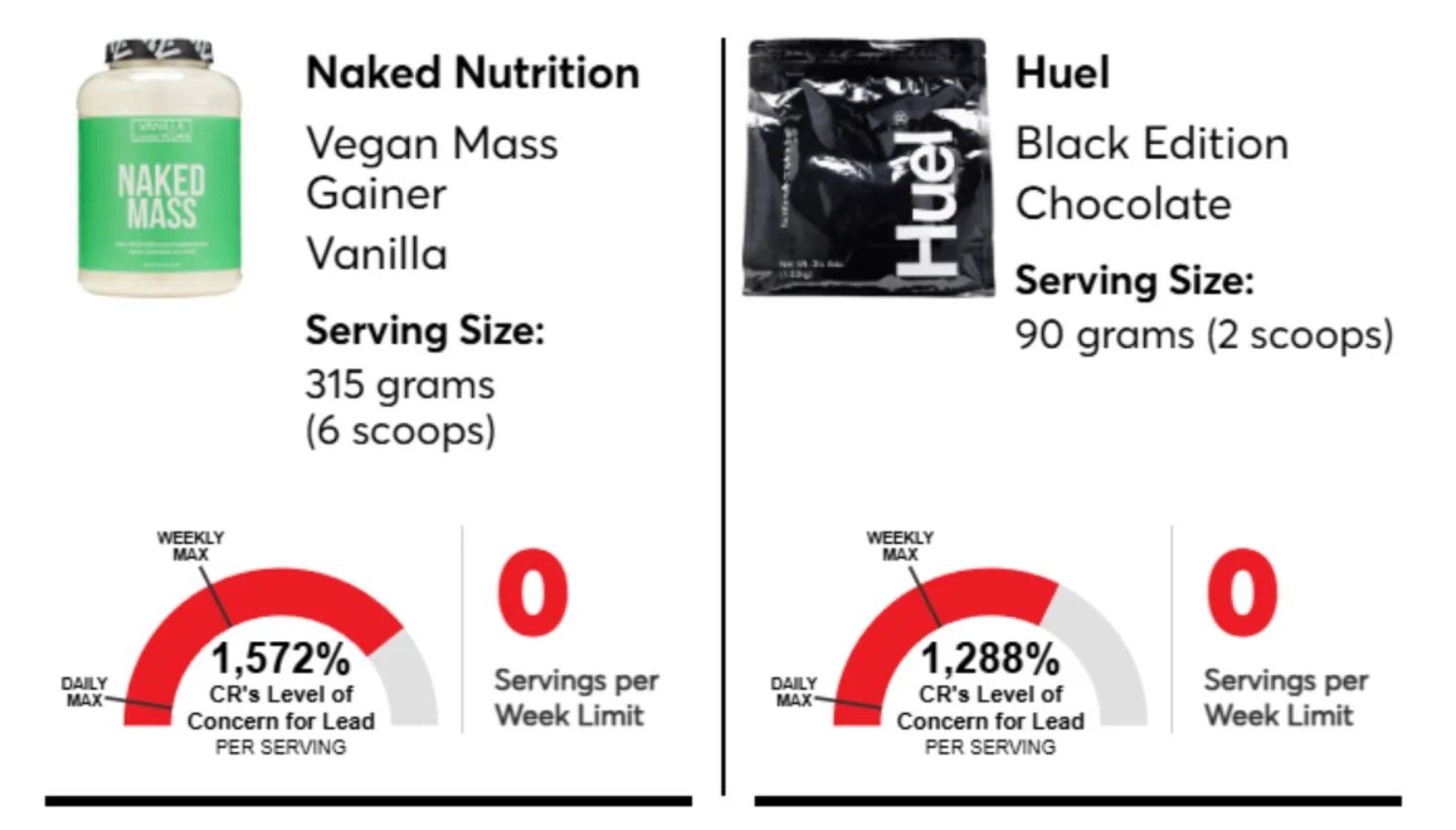

One of the biggest offenders was Huel’s Black Edition Chocolate—a sleekly marketed, premium-priced powder that contained 1,288% of the recommended daily intake of lead.

Another, Naked Nutrition’s Vegan Mass Gain Vanilla, promoted the tagline “ONLY FIVE PREMIUM INGREDIENTS WITH NOTHING TO HIDE,” yet packed 1,572% of the daily lead limit—perhaps that was the unlisted sixth ingredient.

Source: Consumer Reports - "Protein Powders and Shakes Contain High Levels of Lead"

If you’re an active adult, most nutrition research suggests aiming for 0.8–1.2g of protein per kilogram of body weight per day (and up to 2g/kg for athletes). Protein powders can seem like a convenient shortcut to help hit that target—an easy “health hack” on the way to better performance and recovery.

But the CR study is a reminder that shortcuts often come wrapped in sleek branding and confident claims. It’s a reminder that what looks premium isn’t always pure. You have to know exactly what you’re buying and putting into your body.

And that lesson doesn’t stop at nutrition. It applies to investing, too.

Alternative investments—private equity, venture capital, hedge funds, private credit, and more— have moved from the institutional realm into the mainstream. Once reserved for endowments, pensions, and large family offices, these strategies are now being marketed broadly to individual investors.

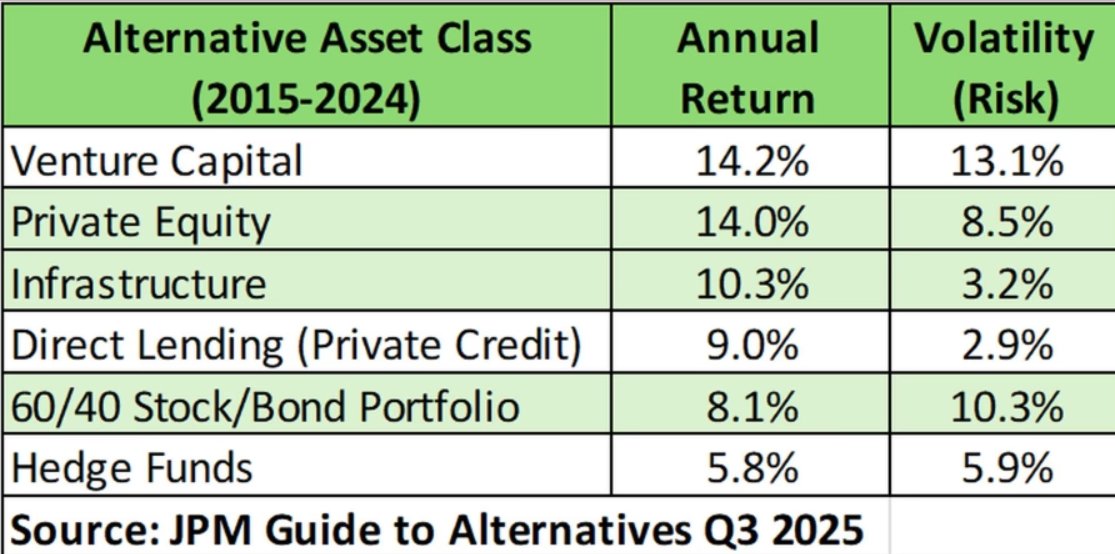

The appeal is understandable. Over the past several decades, the headline returns across many alternative asset classes have been compelling, often matching or exceeding the performance of traditional equities and bonds (such as the classic 60/40 stock/bond portfolio). From JP Morgan:

They’ve also behaved differently. Historically, alternatives haven’t moved in lockstep with the public markets. Because of these distinct correlation patterns, incorporating alternatives into a portfolio has offered the potential not only to enhance returns, but to reduce overall volatility. In investing terms: having your cake and eating it too. (Source - JPM Guide to Alternatives 2025)

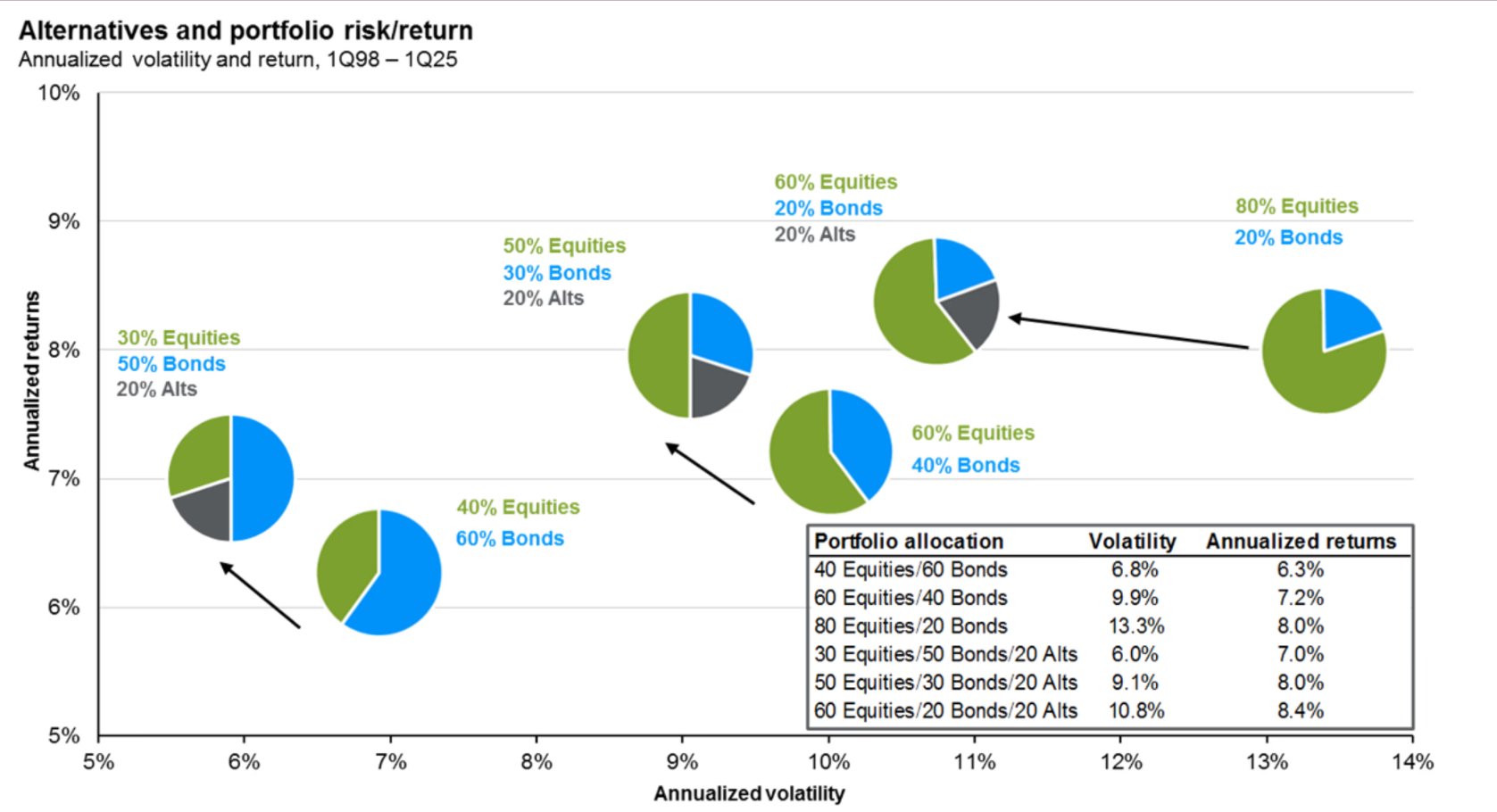

As JPM’s slide shows, from 1998 to 2025, the traditional 60/40 stock/bond portfolio returned 7.2% with 9.9% volatility. Improving upon things, a portfolio mix of 60% stocks, 20% bond and 20% alternatives would have returned 10.8% with 8.4% volatility – an improvement of 3.6% while lowering risk by 1.5% per year.

And then there’s access to innovation. Some of the most dynamic companies in America—SpaceX, OpenAI (ChatGPT), Stripe, Anduril—are venture-backed and privately held. They’re not listed on public exchanges. If your portfolio only holds public equities, you don’t get exposure to companies reshaping aerospace, AI, financial infrastructure, or national defense.

That return profile, and the chance to access innovation and differentiated sources of growth, is exactly why alternatives are compelling. The upside is real. The question is how to pursue it responsibly.

Like health supplements, investors seeking to benefit from alternatives need to approach space with an immense amount of caution and skepticism.

First, there is a massive difference in the quality of alternative investment managers. Unlike public markets, with a few exceptions, you cannot simply “buy the index” and get the asset class return. You have to choose a specific manager (if you can even get access to them), and your outcome will depend heavily on their skill.

And there are a lot of managers to pick from. Take private equity (PE) for instance. Joe Bae, co-CEO of KKR (a well-regarded PE firm), recently pointed out that there are more private equity funds in North America than McDonald’s franchises, roughly 19,000 funds versus 14,000 restaurants. Quantity is not quality.

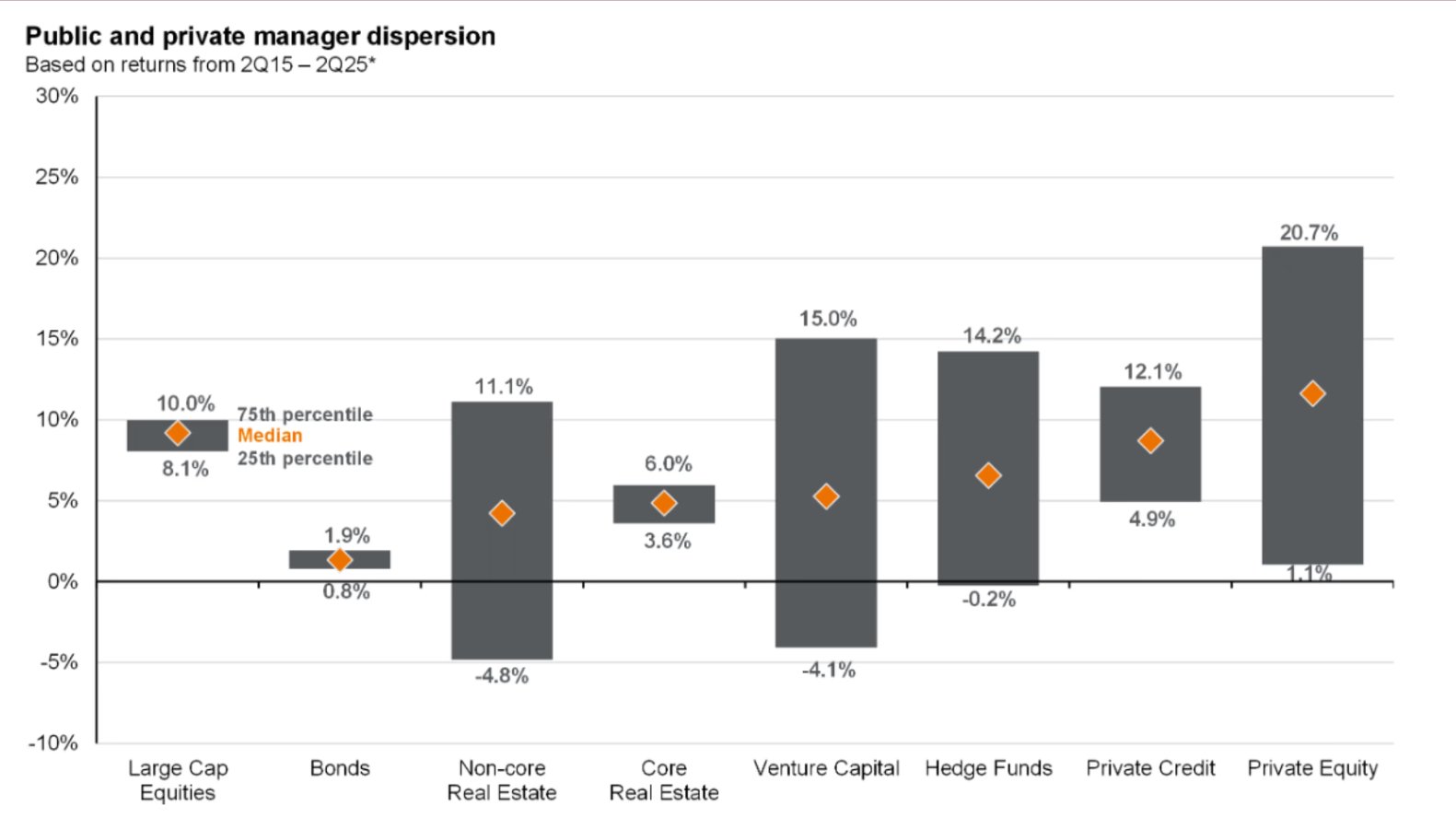

The result? Returns vary dramatically. (Source - JPM Guide to Alternatives 2025)

JPMorgan’s chart makes this clear: the variation between the best and the worst alts managers is nearly 20%. The median return doesn’t tell you what you will get. Your outcome depends entirely on who you pick.

Second, the complexity ramps up quickly when investing in alternatives. Even if you do pick the right manager, the pharma ad like side effects are unavoidable:

· Illiquidity: Capital locked away for 5–15 years, often with no flexibility if life or markets change

· Capital calls: Money sits idle waiting to be drawn, creating drag

· K-1s: Always late. Often require amended returns. More accounting complexity.

· Layered fees: Management + carry + monitoring = 3–4% yearly headwind before alpha

· Opaque valuations: Gains marked to model, not market

· Limited transparency: Sanitized quarterly letters instead of real insights

This is where most investors, and frankly, most advisors, hit the wall. Evaluating alternatives isn’t something you pick up casually. It requires time, repetition, context, and the ability to separate skill from storytelling.

I spent nearly twenty years working inside the alternatives industry. In a typical year, our team might review 400 to 500 manager pitches—and invest in one or two. Not because the others were necessarily “bad,” but because true, repeatable skill is rare. Strong firms have a real sourcing advantage, a clear and consistent investment process, disciplined risk management, and meaningful personal capital invested alongside their clients. Those qualities are harder to find than most marketing suggests.

That experience shaped how I approach alternatives today: with patience, skepticism, and a steady commitment to saying no far more often than yes.

So how do sophisticated investors navigate this space effectively?

They start with real diligence—not marketing decks.

They verify track records across multiple market cycles. They evaluate how decisions were made and how managers behaved in drawdowns. They analyze underlying portfolio companies—not just headline returns.

They demand alignment.

The best managers invest their own money meaningfully. Their fee structures reward results, not asset gathering.

They build portfolios, not one-off bets.

Institutions diversify across multiple managers, strategies, and vintage years. They pace commitments. They manage liquidity, tax exposure, and operational complexity intentionally.

They understand access matters.

The most compelling funds don’t need to advertise. They are selective about their investor base.

And they monitor continuously.

The work doesn’t end once capital is committed. Oversight, communication, and thesis discipline are ongoing responsibilities.

This is the expertise required to invest in alternatives successfully—consistently, across cycles.

Most individual investors don’t have the time, networks, or context to build this machine themselves. That’s not a shortcoming. It’s simply the nature of the asset class.

Alternatives are portfolio supplements. Just like a well-balanced meal delivers the core nutrition you need, a well-built portfolio of stocks and bonds can absolutely help you reach your financial goals. But when added thoughtfully—with genuine research, real expertise, and disciplined selection—alternatives can enhance the journey. They can smooth volatility, provide access to parts of the economy public markets don’t offer, and potentially improve outcomes over time.

But the lesson from the CR study still applies here: what looks premium isn’t always pure, and convenience is not the same thing as quality. Just like supplements, alternatives require scrutiny. Because when you get the right ones—sourced carefully, evaluated rigorously, and held with patience—they can be a powerful complement. When you don’t, they can do more harm than good.

Our role is to help you distinguish between the two.

The goal isn’t to chase what’s shiny—it’s to choose what’s real. Not chasing shortcuts—but building portfolios designed to endure.

Disclosure:

The content provided in this blog post is for informational purposes only and should not be considered as investment advice or a recommendation to buy, sell, or hold any specific security or financial product. The information expressed represents the personal opinions of the author and may not necessarily reflect the views of Bootpack Financial Partners, LLC.

Investing involves risk, including the potential loss of principal. Past performance is not indicative of future results. All investments involve risks, including the loss of principal. There is no guarantee that any investment strategy will achieve its objectives or that it will be profitable.

Before making any investment decision, it is recommended that you consult with a qualified financial advisor who is familiar with your personal financial situation. This blog post may include information or references to specific securities or strategies; however, the author or Bootpack Financial Partners, LLC does not guarantee the accuracy, timeliness, or completeness of this information.

The author may hold positions in some of the securities or investments mentioned, and these positions may change at any time. Neither Bootpack Financial Partners, LLC nor its affiliates are responsible for any losses or damages resulting from the use of this content.