Box Spread Loans - A New Force in Real Estate Financing

*Disclosure: Rates shown are approximate as of April 2026, do not include any additional management or origination fees and are subject to change at any time without notice. Actual rates may vary significantly based on market conditions, borrower qualifications, and other factors, and are not guaranteed. Information presented may be incomplete or inaccurate and should not be relied upon as the sole basis for any financial decision.

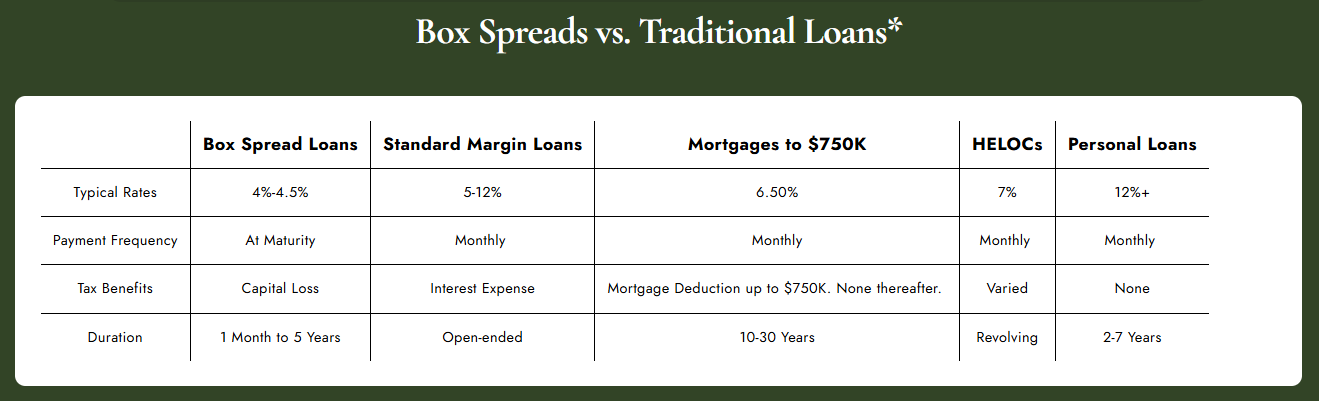

When Selling Assets Isn't the Answer: The Box Spread Loan

The list of blessings in my life is long, among them: buying my house at the tail end of Jackson’s golden age of real estate.

That brief window after the GFC and before COVID when you could still find something under $700 a square foot, watch it sit for a bit, negotiate real contingencies, and lock in a mortgage rate around 3%.

Fast forward to today, and the Jackson market is almost unrecognizable. You don’t need to be a real estate agent to see it: inventory is tight, prices are high, and well-located properties still attract serious competition, especially in the higher end of the market.

Contingencies are rare. Financing can be a disadvantage. If you show up with a 2018 buyer’s playbook, you’re probably not getting the deal.

Then there’s the rate environment. Moving from ~3% to 6–7% doesn’t sound dramatic until you run it against a $3–5 million purchase.

So you end up in a familiar position for many high-net-worth buyers: significant assets, but much of it tied up in a taxable portfolio you’d prefer not to unwind—especially into a volatile market with embedded gains.

That’s where a different approach to financing starts to matter.

The Core Problem

Selling appreciated assets creates a tax bill you’d rather defer

Traditional financing is materially more expensive than it used to be

Winning deals often requires speed and certainty

A different tool: box spread loans

A box spread loan lets you borrow against your taxable portfolio using the options market instead of a traditional bank. When structured properly, it can act as a bridge financing source for a purchase, a complement to a mortgage, or, in select cases, a temporary substitute for traditional financing while waiting on a defined liquidity event.

What’s driving interest right now:

Rates can be meaningfully below conventional mortgages, depending on structure and market conditions.

Terms typically run up to five years, giving you time to refinance, sell, or reposition.

No required monthly interest payments; interest accrues and is settled at maturity.

The “interest” generally shows up as a capital loss, subject to your CPA’s guidance, which can help offset capital gains elsewhere in your portfolio.

In plain English: you can finance a large purchase directly from the market, often at lower rates, without selling your investments—and you control how much of the capital stack runs through this structure.

Two ways to use it

Think about box spread financing along a spectrum:

1. Bridge financing to a defined liquidity event

For some buyers with large, diversified taxable portfolios, a box spread loan can temporarily finance most or all of a purchase when there is a clear liquidity event ahead, such as selling another home, receiving business sale proceeds, or refinancing after closing.

In this case, the box spread is not permanent debt. It is a bridge: a way to move quickly, compete with cash, and avoid selling appreciated assets at the wrong time.

Because terms typically run up to five years, the exit plan matters from day one.

Little or no down payment from cash

Portfolio stays invested

Cash-like certainty at closing

Repayment tied to a specific liquidity event, refinance, or planned portfolio repositioning

2. Hybrid financing: mortgage + box spread

Others prefer to blend tools to keep some traditional bank debt in place and take advantage of what the tax code still gives you. That’s where the $750k number matters.

For many taxpayers, qualified home mortgage interest is limited to interest on up to $750,000 of acquisition debt, subject to IRS rules and individual circumstances.

So instead of financing the entire purchase through a bank, some buyers are using a hybrid structure: keep a traditional mortgage up to the deductible limit, and use a box spread loan for the rest.

On a $3M purchase, that might look like:

$600k cash equity, or 20% down

$750k traditional mortgage, preserving mortgage interest deductibility up to the current IRS cap

$1.65M box spread loan for the remaining financing need

In that setup:

Your bank debt is capped where it may still be tax-favored.

The bulk of the non-deductible, higher-rate financing is replaced with a box spread loan that can offer lower rates, no monthly interest payments, and interest that may function as a capital loss at maturity, again coordinated with your tax advisor.

Structured thoughtfully, you may be able to avoid liquidating a big block of appreciated stock while also avoiding 6–7% interest on financing dollars that may not generate a tax deduction anyway.

Sizing and risk

This is a powerful tool, not a magic trick.

A common starting point is borrowing on the order of 25–30% of a taxable portfolio, but the right number depends on your asset mix, volatility, and overall liquidity. Some buyers may comfortably go higher; others will want more margin of safety.

Key risks to understand:

The strategy requires precise options execution and ongoing monitoring.

Portfolio values can move; a large drawdown can tighten your margin cushion and, in extreme cases, trigger a margin call.

The loan must be repaid or refinanced at maturity, typically within five years.

Structure and tax treatment need to be coordinated correctly with your CPA.

Used thoughtfully, it can create flexibility and an edge in tight markets. Used casually, it can create stress.

Who this works for

This tends to fit buyers who:

Have at least $2M+ in a taxable brokerage account, not retirement accounts

Prefer not to liquidate appreciated assets to fund a purchase

Want to move quickly and compete with cash buyers in a market like Jackson

Have a clear repayment plan, especially when using the strategy as bridge financing

For this profile, box spread financing is essentially institutional-grade liquidity on demand: you can show up like a cash buyer without detonating your long-term strategy.

And the use cases extend beyond Jackson real estate—business acquisitions, bridge financing, or any situation where short- to medium-term liquidity at competitive rates is valuable.

Execution matters

This isn’t something to piece together on your own.

The value is in the details: structuring the options correctly, aligning the borrowing with your overall portfolio risk, coordinating with your CPA on tax treatment, and timing everything alongside a real estate transaction.

Small mistakes here tend to be expensive. Done well, it becomes one of those quiet advantages sophisticated buyers use without advertising it.

Final thought

Most buyers still default to either all cash or a traditional mortgage because that’s what they know.

But in a place like Jackson—where competition is fierce, rates are elevated, and portfolios are often highly appreciated—box spread loans give you another way to play offense.

If you’re looking at a purchase here and want to see what 20%, 50%, or bridge-style full financing could look like on your balance sheet, we’re happy to run the numbers with you.

To see current rates offered by SyntheticFi, click here.

Disclosure: This material is for informational and educational purposes only and should not be considered investment, tax, legal, lending, or real estate advice. Box spread financing involves options strategies, margin borrowing, market risk, liquidity risk, execution risk, and the potential for margin calls or forced liquidation. Terms, rates, availability, and tax treatment vary based on market conditions, account structure, portfolio composition, broker requirements, and individual circumstances. Any tax-related discussion, including the potential treatment of financing costs as capital losses, should be reviewed with a qualified CPA or tax advisor. Borrowing against a portfolio may not be appropriate for all investors. Before implementing any strategy, consult with your financial, tax, legal, and lending professionals.